A product for every member

Personal account

Administration fees help to cover the cost of running the fund. These fees will come out of your accumulation account balance.

Like most superannuation funds we deduct investment fees and transactions costs, typically from investment earnings before they are added to your account balance.

We’re able to keep this fee low because our expert in-house investment team manage a lot of our funds themselves, more than the average super fund.

-

Read the transcript

The information contained in this video is of a general nature only and contains general advice. It’s been prepared without taking into account your individual objective, financial situation or needs. Before making any decision about your super you should consider your personal circumstances, the relevant product disclosure statement and target market determination for your membership category and whether to consult a qualified financial adviser.

You can access a copy of the product disclosure statement and target market determination relevant to your membership category by visiting unisuper.com.au/pds.

This video has been produced by UniSuper Management Ltd. ABN 91 006 961 799. AFSL No. 235907 on behalf of UniSuper Limited, ABN 54 006 027 121 AFSL No. 492806, the Trustee of UniSuper, ABN 91 385 943 850.

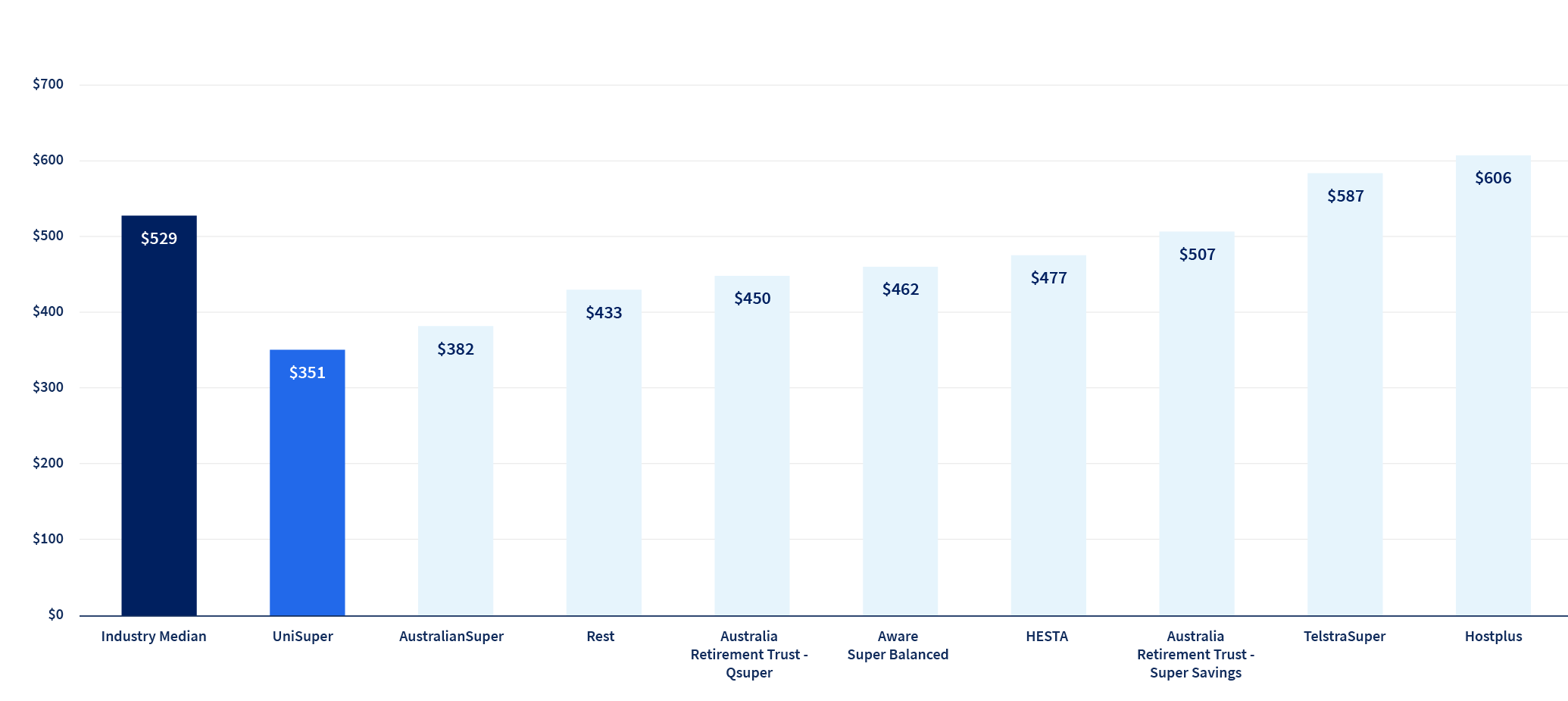

UniSuper might be one of Australia’s largest funds, but our fees are some of the lowest you’ll find.

We’re proud to be an industry super fund. We don’t pay profits to shareholders or commissions to advisers.

There are also no joining fees, contribution fees, or exit fees.

You’ll pay an administration fee for the management of your account. You’ll also pay investment fees and indirect costs for the management of your investments.

If you have insurance cover through your super, you’ll be charged premiums. You should look at the appropriate insurance booklet to find out the exact cost of the premiums.

UniSuper Advice is a financial advice service available to all current and eligible UniSuper members and their families. You’ll receive a quote before proceeding with any service, and you may be able to deduct your fees from your super, depending on the type of financial advice you need and the type of account you have.

You can also find more information on the fees we charge at unisuper.com.au/fees or in your relevant product disclosure statement.

If you have multiple accounts in different super funds, it’s a good idea to compare the fees you pay in each, and consider combining your accounts.

Because even small differences in the fees you pay can add up to tens of thousands of dollars when you retire.

Before combining your super, consider the possible effects this might have on things like the fees you pay, your insurance and the tax on your super. There may be other effects too so it’s best to seek financial advice if you’re unsure. If you’re not a UniSuper member and want to join, see if you’re eligible by visiting unisuper.com.au/join.

And if you have questions about fees or anything else, chat with one of our online consultants during business hours or call us on 1800 331 685.

How our fees compare

Source: Chant West1

What your fees might look like

| Example Balanced (MySuper) option | Balance of $50,0004 | |

|---|---|---|

| Administration fees and costs | The lesser of $96 or 2% of your account balance per year3. | An administration fee of $96 will be deducted from your balance. |

| PLUS Investment fees and costs | 0.42% p.a.3,5,6,7 | And, you will be charged or have deducted from your investment $210 in investment fees and costs. |

| PLUS Transaction costs | 0.09% p.a.5,7,8 | And, $45 will be charged or deducted from your investment in transaction costs. |

| EQUALS Cost of product | If your balance was $50,000 at the beginning of the year, then for that year you will be charged fees and costs of $351 for the superannuation product. | |

| Different investment options have different costs, for a full breakdown see the Investment costs page. | ||

-

Things you need to know

1Source: © Zenith CW Pty Ltd (Chant West) (ABN 20 639 121 403) 2024. This comparison has been prepared by UniSuper using Chant West’s Member Outcomes Dashboard and is based on information provided by third parties that is believed accurate at the time of publication. Fees are as at January 2024. Fees may change in the future which may affect the outcome of the comparison. The above fee comparison is for the UniSuper Balanced investment option only and other funds’ options with similar risk profiles – Chant West’s Growth category (61%-80% growth assets). Fees are compared for a member balance of $50,000. Administration and investment fees and costs data is adjusted by Chant West so like comparisons can be made. Adjustments result in fees being gross of income tax, Investment fees and costs include fees charged (including performance fees) and any transaction costs and accordingly data contained in the research may differ from data shown in other published materials.

2Additional fees may apply. If your account is invested in investment options other than the Balanced investment option, the investment fees and costs and transaction costs will be different to those above. Refer to ‘Additional explanation of fees and costs’ in the product disclosure statement of your relevant product.

3If your account balance is less than $6,000 at the end of UniSuper’s income year, certain fees and costs charged to you in relation to administration and investment are capped at 3% of the account balance. Any amount charged in excess of that cap must be refunded.

4The calculated amounts do not include contributions that may be made during the year.

5The investment fees and costs and transaction costs shown above are indicative only and are based on the investment fees and costs and transaction costs for the year ended 30 June 2023, including several components which are estimates. The actual amount you’ll be charged in subsequent financial years will depend on the actual fees and costs incurred by the Trustee in managing the investment option. Investment fees and costs include an amount of 0.03% for performance fees. The calculation basis for this amount is set out in the product disclosure statement.

6Refer to ‘Additional explanation of fees and costs’ in the Fees and costs document at unisuper.com.au/pds.

7The investment fees and costs and transaction costs for other investment options are set out in the Fees and costs document. They are calculated on the same basis and paid at the same frequency and in the same manner as the Balanced investment option.

8For the financial year ended 30 June 2024, the transaction fees and costs for this option are expected to increase by 0.07%.