Disclaimer: This webcast discusses UniSuper’s investment performance and recent investment decisions designed to suit UniSuper, which may not be appropriate for you personally. We’re not suggesting you should make the same decisions.

Consider your situation and read the relevant Product Disclosure statement before making personal decisions about your investments or UniSuper membership. Past performance is not an indicator of future performance.

Derek Gascoigne (GC): Hi, I'm Derek Gascoigne, a senior adviser in our Melbourne office. Not surprisingly, we've been contacted by a number of members in relation to their concerns about the collapse in share markets and the impact on their superannuation savings. So I'm here with John Pearce, our Chief Investment Officer, to get a current update on the status, the outlook, and the impact on UniSuper's investment strategy. John, can we start with the magnitude of the market reaction we're seeing?

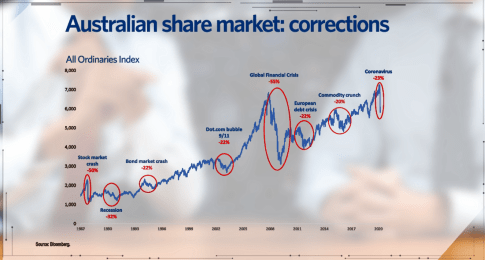

John Pearce (JP): It's a bit of a moving feast as you can imagine, Derek, and it will change by the time this video is aired. I think it's best to think about it from the peak to the trough in this latest selloff. Major markets, including Australia, are down about 20%. We have this graph in front of us here showing the latest decline. And a couple of points here, we are now in official ‘bear’ territory. You'll hear about people talking about a ‘bear market’. What I say to members when you hear that is, don't pay much attention. It's just a label, and the label ‘bear market’ doesn't say anything about the future—it just tells you that the market's down 20%. The other point is that these corrections are a lot more frequent than people might suspect. In fact, since the '80s, it's happened about eight times.

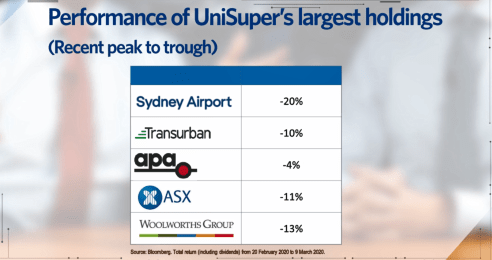

We also have to bear in mind that we've had 10 consecutive positive years. So it's almost the correction that we had to have. Let's look at UniSuper's situation. I'm sure that's what our members are more interested in. If you look at the performance of our five key holdings listed on this slide, you can see, not surprisingly, Sydney Airport has been the hardest hit of our main holdings. It’s pretty much fallen in line with the market, which I take some comfort from, actually—you'd expect it to even fall more given the draconian sort of measures that governments have put in around travelling.

You look at APA, Transurban, ASX, etc., they've all performed better than the market. And I think that's a real testament to how strong the underlying businesses of these companies are.

Let's look at our investment options—in particular our growth options because as you'd expect, our growth options have been adversely impacted. Our Balanced option, which is our default option for accumulation members, from peak to trough, has fallen about 9%.

Now, that's a reasonable fall. But once again, let's take things in context here. If we look at financial year to date, the Balanced option is down about 1%. So pretty flat.

So, despite the magnitude of the fall that we're seeing, given the diversification of the Balanced option, we’re still looking at a flattish result for the financial year. But who knows what's going to happen over the next few months.

We all know what's created the panic, it's obviously the impact of the coronavirus and the economic dislocation arising from that. It's also been exacerbated by a crash in the oil price. Why has this happened? Well, at a time when we want global leaders to really sit down and cooperate to get through this crisis, we're seeing the Saudis and the Russians playing chicken and threatening to increase the supply of oil. That crash in the oil price has then extended fears of potential corporate collapses in the energy industry and contagion impacts from that. So we've got, really, the makings of a perfect storm in the market size.

DG: Do you believe the market movements we are seeing are justified or are they an overreaction?

JP: It's interesting isn't it, because in February, when we cut a video, I made the point that I was astounded at how complacent the market was. There was an outbreak of the virus, the news was pretty negative in my eyes, and you had a situation where a couple of markets were even up at the time. So we've moved from complacency to yes, I believe now the markets have overreacted. And what are the grounds for my view on that? The first fundamental is the science of it all. Now, my team and I aren't experts on viruses or pandemics, but at times like this, we do have to read whatever scientific information is available so that we can actually form a base case.

And the best I can gather, on the consensus available is yes, this is indeed an insidious disease. But one way of putting it is it's the flu on steroids. I'd like to refer our members, if you're interested in actually reading up a lot more about this, one of the best videos that I've seen is an interview with Dr. Steven Ostroff. And we will provide that link on the website. It is long, but I found it very informative and somewhat reassuring.

Let's move on to the other fundamentals. The market is now pricing in a pretty severe recession and a long recession. But that's not the experience of previous types of epidemics or pandemics. What we see is the economic impact is quite short and sharp. And that's particularly if the governments and central banks all get together and work towards solving the problem. We've seen central banks very quickly lowering rates, we’ve seen governments talking about fiscal easings, and we see governments putting in really strong measures in terms of controlling the actual virus—social distancing, bans on travel, etc. So that's the broad macro picture.

What about the company picture? Think about a company like BHP. From peak to trough, BHP had lost nearly 30% of its market value. We just don't accept that BHP was worth a third less than it was four or five weeks ago, particularly when you think about how committed the Chinese are to getting that economy kickstarted. So yes, will BHP take a hit to current earnings? Absolutely. Will this be a long, drawn-out process whereby BHP's earnings are forever impaired? We're just not buying that.

DG: So what you're saying is this is no GFC.

JP: It’s no GFC and those who are suggesting it's a GFC, I suggest you discount a lot of that. Now, let's not trivialise the human cost impact of this. During the GFC, people were not fearing for their lives. In this pandemic or epidemic, people are, so I'm not trivialising that. But from financial and economic standpoint, we are a long way from a GFC-type situation here. Recall that during those times, the global banking system was on the brink of collapse, was on the brink of nationalisation. Now banks today are in a very, very healthy position. They're ready to extend credit to make loans. To me, it's more of a question of confidence and demand for credit, not the supply of credit. We believe it's going to be short-lived. We can, of course, run the risk of talking ourselves into a bigger crisis than it has to be. It could be that the biggest fear is that of fear itself.

DG: So what are you looking forward to signal a turning point? And do you see any light at the end of the tunnel here?

JP: I think there are two pre-conditions that have to be met to see a turning point. The first one is that we have to see evidence of market capitulation. That is, those investors that have borrowed too much, those investors that have to hedge portfolios, the program traders, and people who are generally worried for their own health and are panicking out of things. I think we've seen evidence that that condition has been satisfied.

The second condition, of course, and most importantly, we have to go past the point of peak infections. There's some really good news and some bad news on this. The good news is China. On Monday, we saw new infections in China of 19, of which 17 were in the Hubei Province, which is obviously the epicentre of this issue. Now, bear in mind at its peak, these were running in the thousands in China. So, that country has done an incredible job at controlling the situation. In terms of recoveries within the Hubei Province itself, the recovery rate is about 75%. And in China, outside of that province, it's around 95%. So, once again, more positive news.

Of course, the bad news is that outside China, the rest of the world, infections are on the increase. It's around 4,000 or 5,000 a day, and we've seen Italy being the most affected lately.

I think Italy recently recorded a daily new infection rate of around 1,800. And they're putting in fairly draconian measures in terms of shutting down Italy effectively to try and control that. Of course, the big country to watch over the next 10 days is going to be the USA which, quite frankly, has been a bit of a laggard when it comes to testing. By Friday, the US will have four million test kits available. It's absolutely guaranteed that the infection rate in the US will be spiking. Now, everyone should understand this, everyone should expect this, the market should not overreact when we do indeed see a spike in infections in the US, but markets, as we know, behave in strange ways.

DG: With respect to UniSuper's investment strategy, how have we dealt with the market rout?

JP: We are in incredibly strong position, Derek. We've got elevated levels of cash holdings. And it's not because we had any foresight that this was going to happen, we're not that smart. We were, however, building up cash levels because the market was getting a bit more expensive and we just didn't really see the bargains to allocate the cash. Now, what does that actually mean in terms of a situation like this? Firstly, we've got cash to take advantage of bargains when we see them now, and there's more and more bargains appearing.

Secondly, we're able to manage member-switching very, very smoothly. Let me tell you exactly what I mean. On the graph in front of you, we have the switching behaviour of members over the recent past. What have we seen? To date, about $1.3 billion of money flowing out of our growth options into our defensive options. You can see the big ones there—big outflow from the Balanced option, big inflow to the Cash option.

Now, how do other funds have to handle this? Well, a lot of them have to actually just sell on market. Because a switch out of a growth option is effectively a redemption. A member is effectively asking you for cash. At UniSuper, because of our high levels of liquidity, we don't have to do anything in the market. We can simply fund that through our own cash levels. It's a very fortunate position because it means that we have not had to sell into a distressed market.

DG: So, John, are there some final comments that you'd like to communicate to our members?

JP: Well, ultimately, the comment that we always like to leave with is you stay the course. But we do have to be cognisant that across our member base, we have a lot of people in varying financial circumstances. And let's break them down. Defined Benefit Division members. Well, defined benefit members are in that fund for peace of mind. We estimate the defined benefit, vested benefit index to be around 117, and the accrued benefit index to be around 125 after we've seen this market crash. So you're talking about very, very strong funding levels. So, that peace of mind that you're in the defined benefit for, we believe that we can deliver it.

Accumulation members with a long time before they retire—this is absolutely nothing to worry about. In fact, in a paradoxical sort of way, we've got to welcome these corrections. Because what you're doing is you're effectively buying assets at cheaper prices. And the last thing an accumulation member needs is to keep on buying assets at higher and higher prices.

But what about retirees or pre-retirees? Well, firstly, the main message we give them is seek advice. And I think you know this better than me, but my understanding is that most of our advised clients do have a pot of cash to draw from in times like this rather than having to realise assets in a weak market. But I think even our retired members that have to access their capital, we've got diversified portfolios and the response of these portfolios during the GFC, for example—when we had the worst financial crisis in 100 years—was pretty reassuring. Our Balanced option post the GFC took about three years to recover all of its losses. It recovered 50% of its losses in as low as seven months. So when you think about yourself as a retiree, you're obviously not having to sell everything to fund your lifestyle, it's usually a very small component. As a diversified portfolio, we expect a reasonably quick recovery as well. So I think that's reassuring.

The final point I'd like to make—it’s times like this when you might have some regrets. You might be thinking, "Gee, if only I sold three or four weeks ago, I'd have been so much better off today." That's a natural reaction, we all think that way. But bear in mind, you’ve got to get back in—otherwise you miss out on the upside.

I stumbled upon this bar chart here that I think illustrates the point really well. Here's the performance of the American stock market over a 20-year period starting 1999. You invest $10,000. The return is about 5.6% if you stayed in that whole time. What if you just missed the best 10 days over that 20 years? That return collapses to 2%. What if you actually just missed the best 20 days? You're now talking about a negative return.

So you see why we come back to that old adage—time in the market is always better than timing the market.

DG: Thanks, John. If you have some questions that you'd like answered, please email us at superinformed@unisuper.com.au. Thanks for watching.

Disclaimer: Information on this web channel, including accessible video content, is provided by UniSuper Management Pty Ltd. Trustee: UniSuper Limited (ABN 54 006 027 121, AFSL No. 492806). Fund: UniSuper (ABN 91 385 943 850) Administrator: UniSuper Management Pty Ltd (ABN 91 006 961 799, AFSL No. 235907).