Choosing the right super fund for you usually means finding a fund that suits your current and future needs. You’ll typically look for:

- strong long-term performance and low fees

- investment options that suit your needs

- member services, insurance options and financial advice

-

Read the transcript

Comparing super funds

There are good reasons to regularly compare super funds.

Firstly, not all super funds are the same, and what's on offer can change over time.

Similarly, what you need out of a super fund can shift as your circumstances change.

Ideally, you should compare super funds before your first job, as well as at key life intervals like getting a promotion, buying a home, and approaching retirement.

There are three things to consider when comparing super funds: the range of investment options on offer, specifically those that appeal to you; features like member services, insurance options and financial advice; and your 'net benefit', which is your investment returns minus fees and costs.

There are two key things to consider when you're looking at performance. Look at results over a 5-10 year period to get a sense of how consistent a fund's returns are. Make sure you're comparing apples with apples. Always compare the investment options you're interested in with similar options from other funds.

Keep an eye out for fees related to administration, insurance, investment options, and account-based fees such as switching or withdrawal fees.

Higher risk options usually provide higher returns, but they come with greater risk. Depending on your circumstances, a lower risk option might be a better choice.

At UniSuper, you can find investment options that suit your needs. We have pre-mixed options where we do the work for you. We have individual sector options where you can build your own portfolio. You'll also find sustainable and environmental branded options, which typically limit exposure to certain sectors.

For more information on how UniSuper stacks up against the competition, visit unisuper.com.au/compare.

Understanding your net outcome to help you compare your super#

This table compares the net outcomes of UniSuper’s default Balanced (MySuper) investment option and the median net outcomes of comparable options for ‘retail master’ funds and the ‘industry’ overall.

On this basis a UniSuper member invested in UniSuper’s Balanced option would be $18,274 better off over 15 years than the industry median, and $37,301 better off than the retail master trust median.

| Net outcome 1 Yr |

Net outcome 3 Yr |

Net outcome 5 Yr |

Net outcome 7 Yr |

Net outcome 10 Yr |

Net outcome 15 Yr |

|

|---|---|---|---|---|---|---|

| UniSuper’s Balanced investment option | $5,258 | $9,371 | $26,326 | $40,070 | $73,177 | $169,358 |

| Retail Master Trust Median | $5,313 | $8,677 | $21,537 | $31,538 | $56,638 | $132,057 |

| Median | $5,144 | $9,833 | $23,168 | $34,432 | $62,222 | $151,084 |

Net outcome refers to investment earnings to 31 December 2023 (less administration and investment fees and costs)

Source: SuperRatings Net Benefit report for 31 December 2023, data extracted on 21 February 2024.

-

Important information about Net outcome

#Source: SuperRatings Net Benefit report for 31 December 2023, data extracted on 21 February 2024. This table compares the net outcome of UniSuper's default Balanced (MySuper) investment option and the other funds' balanced options with a similar risk profile. It assumes employer contributions on a starting balance of $50,000 and annual salary of $50,000 and takes into account historical investment earnings (after administration and investment fees and taxes). Net outcome refers to investment earnings to 31 December 2023 (less administration and investment fees and costs). Past performance is not an indicator of future performance.

The SuperRatings net benefit calculation assumes the following:

- a starting super balance of $50,000

- an annual starting salary of $50,000

- salary growing at 3.5% p.a at the end of each year

- applying effective annual returns at end of each financial year

- after-tax quarterly SG contributions made at the end of each calendar quarter, and is based on actual SG contribution rates of the relevant year

- contribution tax of 15%

- fees and investment returns determined annually based on data from product disclosure statements.

The assumption does not consider any additional salary sacrifice or voluntary contributions, nor the cost of insurance premiums.

Comparing performance

There are a few ways to find how a fund performs.

Look at long-term results

By looking at results over a five to ten-year period, you can get a sense of how consistent a fund is with their returns.*

Determine risks and returns

Higher risk investment options generally provide higher investment returns over the long term but may not be suitable for everyone.

Compare apples with apples

Always compare your preferred investment option with similar options.

Comparing fees

Fees and costs can make a big difference to your retirement outcome over time. When you’re comparing, see how much you’ll pay for administration fees, insurance, your preferred investment options, and account-based fees, such as switching or withdrawal fees.

You may also be paying for how a fund manages your super. We keep our fees low by managing over 70% of our investments in-house and ensuring profits stay with members, rather than shareholders.

Our Balanced Investment option fees compared

| Account balance | Ranking for lowest fees |

|---|---|

| $500,000 | 2 |

| $250,000 | 2 |

| $100,000 | 2 |

| $50,000 | 3 |

-

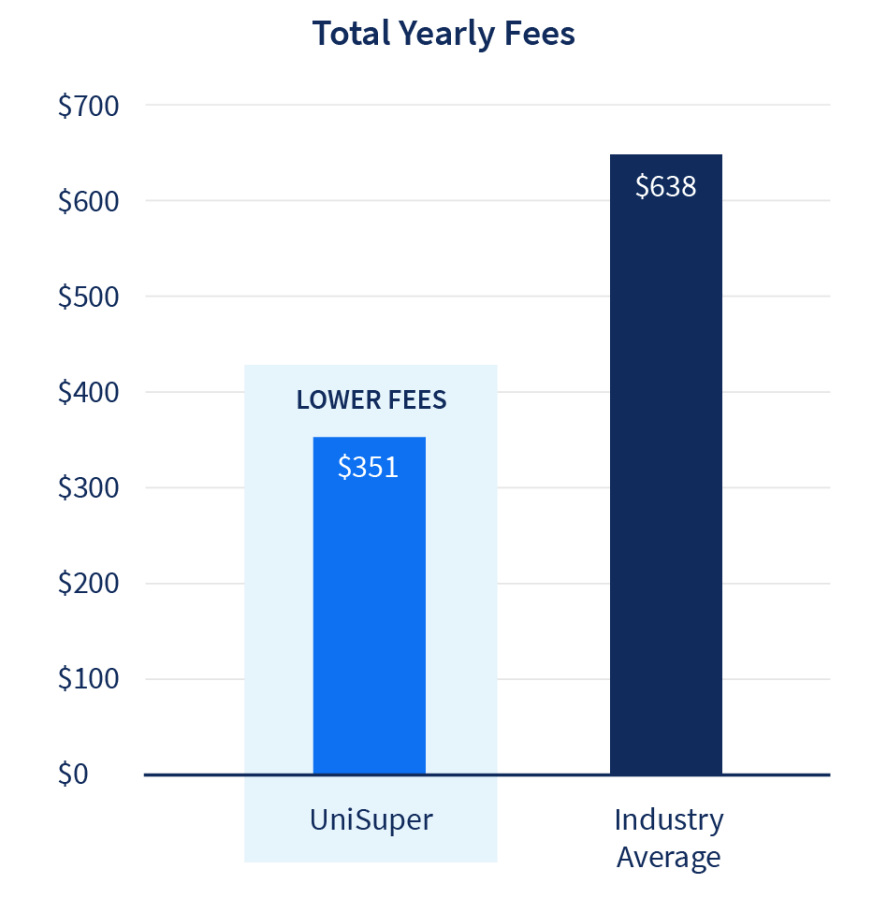

What your UniSuper fees might look likeIf you had a super balance of $50,000 in a Balanced (MySuper) investment option, your annual fee breakdown could look something like this:2

Balanced (MySuper) option Balance of $50,0003 Administration fees and costs (the lesser of $96 or 2% of your account balance) $96 Investment fees and costs4 5 $210 Transaction costs (0.08%)3 4 10 $45 Total $351 Other things to consider:

- Compare the investment option you’re interested in — each option has its own set of internal and external fees, which makes the fee you pay variable.

- The above guide doesn’t account for circumstantial account-based fees such as switching or withdrawal fees.

For more information, download our Fees and costs booklet (PDF, 460KB).

Compare us with other Australian superannuation funds

Discover how a superannuation fund invests

Understanding how a fund invests can help assure you your super’s in good hands. By managing over 70% of funds in-house, we’re able to deliver long term returns and keep our fees low.6 But that’s not the only way we make investing better for members.

Accessibility

Prefer a less active approach to managing your investments? Pick one of our

Flexibility

If you’re a more hands-on investor, you can build your own portfolio. Choose from our diverse selection of Sector investment options.

Environmental, social and governance7

We consider key environmental, social and governance factors across our major investments. We also offer members two sustainable branded investment options and an environmental branded option.

Get the UniSuper app

Manage your account from wherever you are 24/7. Check your estimated balance, review your investment options, keep up with recent transactions and more.

We’re known as one of Australia’s most awarded super funds

Super fund comparison FAQs

-

How do I compare insurance cover from super funds?

Getting insurance through your super fund could be an affordable way to get important covers, such as death, total and permanent disability (TPD) and income protection cover. Factoring insurance into your comparison is important because premiums are taken out of your super, so expensive cover can cost you over time.

When comparing insurance offered by super funds, factor in:

- the cost of your premium

- the amount of cover included

- Any exclusions, definitions or restrictions that apply to you.

-

How do I compare financial advice services from super funds?

If you’re interested in managing your money or are planning for retirement, comparing funds’ financial advice services could pay off down the track. Consider what sets offerings from funds apart, and if there are any services that speak to you.

For example, our financial services team:

- is run in-house, rather than a third party

- offers more locations for face-to-face meetings with members across Australia

- doesn’t receive incentives or commissions for products or services they recommend

- will recommend another fund if it’s in your best interest or you’d prefer your super elsewhere.

-

How do I transfer my super to UniSuper?

You can bring your super over to us in three easy steps using our combine super tool.9

- Log in to your account to use the combine my super tool.

- Verify and search to find any other super accounts you may have.

- Select the account you want to combine.

-

What should I consider before transferring my super?Before combining your super, consider any impact the possible effects this might have on your personal situation.9 This can change from person to person, but can include things like:

- the fees you pay

- your insurance

- super-related taxation.

-

Things you need to know

This information is of a general nature only and does not take into account your individual objectives, financial situation or needs. You should read the product disclosure statement and booklets relevant to your membership category, consider the appropriateness of the information having regard to your personal circumstances and consider consulting a licensed financial adviser before making an investment decision based on information contained here.

1Source: © Zenith CW Pty Ltd (Chant West) (ABN 20 639 121 403) 2023. Chant West Super Fund Fee Survey December 2023 comparing administration and investment fees and costs of the UniSuper Balanced investment option as ranked in Chant West’s Growth [61-80%] investment risk category against 74 similar investment options for other funds within the same investment risk category. Administration and investment fees and costs data is adjusted by Chant West so like comparisons can be made. Adjustments result in fees being gross of income tax, administration fees and costs include all administration-related fees and costs including costs paid from reserves, investment fees and costs include fees charged (including performance fees) and any indirect costs and accordingly data contained in the survey may differ from data shown in other published materials. The comparison is for the UniSuper Balanced option only – rankings may differ for other investment options. Fees may change in the future which may affect the outcome of this comparison.

2Additional fees may apply. If your account is invested in investment options other than the Balanced investment option, the investment fees and costs and transaction costs will be different to those above. Refer to ‘Additional explanation of fees and costs’ in the product disclosure statement of your relevant product.

3The calculated amounts do not include contributions that may be made during the year.

4The investment fees and costs and transaction costs shown above are indicative only and are based on the investment fees and costs and transaction costs for the year ended 30 June 2023, including several components which are estimates. The actual amount you’ll be charged in subsequent financial years will depend on the actual fees and costs incurred by the Trustee in managing the investment option. Investment fees and costs include an amount of 0.03% for performance fees. The calculation basis for this amount is set out in the product disclosure statement.

5The investment fees and costs and transaction costs for other investment options are set out in the Fees and costs document. They are calculated on the same basis and paid at the same frequency and in the same manner as the Balanced investment option.

6Past performance is not an indicator of future performance. Consider the PDS and TMD on our website and your circumstances before making decisions, because we haven’t. Read the full disclaimer.

7Sustainability and environmental investing mean different things to different people. Different products have different investment criteria. Read our website and PDS to find out what sustainable and environmental investing means to us and what our products invest in.

8Zenith CW Pty Ltd ABN 20 639 121 403 AFSL 226872/AFS Rep No. 1280401 Chant West Awards issued 17 May 2023 are solely statements of opinion and not a recommendation in relation to making any investment decisions. Awards are current for 12 months and subject to change at any time. Awards for previous years are for historical purposes only. Full details on Chant West Awards at https://www.chantwest.com.au/fund-awards/about-the-awards.

9Before combining your super, consider the possible effects this might have on things like the fees you pay, the conditions of your insurance (including whether you can transition your insurance in your other fund to UniSuper) and the tax on your super. There could be other effects too, so it’s best to seek financial advice if you’re unsure.

10 For the financial year ended 30 June 2024, the investment fees and costs for this option are expected to increase by 0.07%.

11 The rating is issued by SuperRatings Pty Ltd ABN 95 100 192 283 AFSL 311880 (SuperRatings). Ratings are general advice only and have been prepared without taking account of your objectives, financial situation or needs. Consider your personal circumstances, read the product disclosure statement and seek independent financial advice before investing. The rating is not a recommendation to purchase, sell or hold any product. Past performance information is not indicative of future performance. Ratings are subject to change without notice and SuperRatings assumes no obligation to update. SuperRatings use proprietary criteria to determine awards and ratings and may receive a fee for the use of its ratings and awards. Visit superratings.com.au for ratings information. © 2023 SuperRatings. All rights reserved.